After a long hibernation not unlike the seasonal preoccupation of the polar bear,YTL Corporation has stirred into some volume action.

I was away for the last two days and have not been keeping up with the Bursa action when I was told that YTL has cross into the RM1.50 price territory.

When an acquaintance told me about it, I was nonplussed as my average price was RM1.55 and that development was not really comforting.

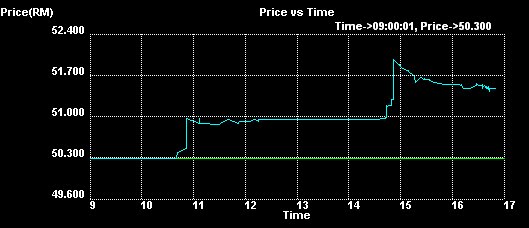

This morning, it spurted passed the RM1.60 price on huge volume with some deals done in 100,000 tranches.

What is brewing in YTL as it is neither GAB or Carlsberg? And certainly not from heavy smoking in BAT?

What is Francis up to this time?

After taking YTL Cement off the board and compelling every shareholder possible to convert to YTL shares, he will be using his legal avenues to wrestle away those stubborn YTL Cement shareholders who refuse to part with their YTL Cement shares.

YTL Corp Bhd is a good share.

For its second quarter of its current fiscal year ended Dec 31, 2011, it posted a 44.6% year-on-year jump in net profit to RM237.4mil as compared with RM164.2mil a year earlier. YTL Corp and its listed arms' financial year ends on June 30, 2012.

For the quarter under review, the well-diversified group's revenue increased 18.4% year-on-year to RM5.3bil.

Francis informed the Group continued to perform well due mainly to the “ongoing resilience of our multi-utility businesses in Malaysia, Britain and Singapore”.

“Our cement and multi-utility operations, which are the group's major contributors, continue to register sound performance,” he added.

For the six months ended Dec 31, 2011, YTL Corp recorded a 10.4% year-on-year jump in net profit to RM489.2mil while revenue increased 10.8% to RM9.87bil.

Meanwhile, for the first half of FY12, YTL Power International Bhd's net profit grew 5.2% year-on-year to RM560mil while revenue rose 9.4% to RM7.7bil, due mainly to better performance of its merchant multi-utility businesses.

However, the division's YES mobile broadband operations registered a loss due mainly to the upfront implementation costs to build the 4G network for scale in order to cover the peninsula.

YTL Cement Bhd saw its net profit for the first half of FY12 grow by 8.8% year-on-year to RM167.9mil while revenue increased 12.2% to RM1.15bil due mainly to higher demand for cement in the construction industry and contributions from offshore subsidiaries.

On YTL Power, analysts said the company's results for the first half of FY12 were within expectations.

According to CIMB Research,YTL Power has a cash horde aimed for suitable mergers and acquisitions it can find.

“We believe YTL Power would eventually win the national 1Bestarinet smart school project. The project is worth RM300mil per annum over 10 years,” said CIMB Research. This is most interesting, don't you think? A certain little bird is up to no good?

Meanwhile, HwangDBS Vickers Research pointed out that YTL Power's dividend per share was lower quarter-on-quarter.

The research house said this was possibly because the company wanted to retain cash to fund increasing capital expenditure for YES, and potential investments in new power plants in Malaysia and overseas regulated assets.

YTL Power had declared a 1.875% or 0.9375 sen per share second interim dividend for FY12.

So, what do you think is brewing at YTL.

There will be no need for another share split. After the share exchange with YTL Cement shareholders, there is definitely a certain glut of YTL shares in the market.

Even the buying for Treasury shares is fast approaching the 10% legal limit.

So what can one expect from this sudden flurry of buying apart from possible Treasury buys?

Share redistribution

in specie to loyal shareholders? Very likely.

At the close, YTL Corp became the most traded counter rising a spectacular 17 sen to RM1.75 on a volume of almost 12 million shares.

I think besides the Treasury buy-ins, other parties both speculators and institutions from at home and abroad could have jumped onto the counter on some expectations of positive corporate development.

Who knows?