If so, what are their possible logical reasons?

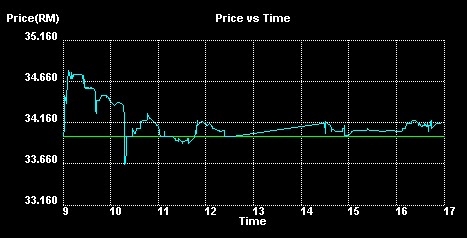

Right now, Digi shares are skirting below the RM34.50 price divide. The highest it did was RM34.54 about a hour ago. It has touched RM35.00 in earlier trading sessions. Will it once again touch RM35.00 or even go beyond in the next few days?

At noon, Digi shares closed at RM34.52 with plenty of buyers in tow at RM34.50. It gained 74 sen at half day trading halt. Market willing,it appears that the shares might just end at or above RM34.50 today. As expected, it ended at RM34.52 with a gain of 74 sen intact even though it breached RM34.56 at one point.

At the recent EGM, the Chairman said that the shareholding spread is very small as Digi itself holds 49% of it. They intend to buy some more once the government approves the liberalized framework and that could be sooner that we can expect.

Anticipating this, I am sure punters are picking up Digi stocks and friendly parties could also be accumulating. Once the shares go ex;say at RM3,50; that will allow more minority shareholders like the man in the street to procure shares in trading lots of 100s and 200s to share in the growing story of Digi. And that may also trigger institutions from both external and internal to start mopping loose split lots.

My take is it will be a matter of time before Telenor buys into the market. That will tighten the share-spread once more to propel Digi shares to go beyond possibly RM4.00.

I also believe Digi will also be having a 10% share buy back facility at the next AGM in 2012.

We await for this kind of scenario to unfold before 2011 ends.